In May, the Fed raised interest rates for the second time in two months. Could we see more aggressive rate raises in the near future — and how will they impact investors?

Overview

After keeping the federal funds rate near zero for the better part of two years, the Federal Reserve decided in March it was time to take action against inflation. It nudged rates upward by 25 basis points (0.25%), moving the target rate to 0.25% – 0.50%. The Fed increased rates again at its May meeting, this time making a bigger jump of 50 basis points (0.50%) for a target rate of 0.75% – 1.00%.1

Fed Chair Jerome Powell announced the latest increase following the meeting. He also indicated the Fed’s intent to keep raising rates to 50 additional basis points in both the June and July meetings. After initially celebrating this announcement, the next day markets decided they didn’t believe Chairman Powell’s words, and stocks dropped. By May 5, futures on the federal funds rate priced in a 75% chance of the Fed raising rates by 75 basis points in June.2

Why is the market paying such close attention? Let’s take a look at what the federal funds rate is and how shifting the rate can directly impact markets and individual consumers.

Understanding the Federal Funds Rate

The Federal Reserve’s primary mandates are setting monetary policy and promoting stability of the financial system in the U.S. One of the ways it does this is by setting the federal funds rate — the target rate established by the Federal Open Market Committee (FOMC). But while this rate serves as a guidepost for commercial banks as they borrow and lend excess reserves, the real rate is based on supply and demand in the overnight lending market.

The Fed shifts the federal funds rate to help promote (or discourage) economic growth. Keeping rates low encourages borrowing, which spurs individual consumers and companies to spend more and results in an expanding economy. The inverse is also true: Raising rates means fewer loans and less spending, eventually leading to a contracting economy.

Where Rates Have Been — and Where They’re Going

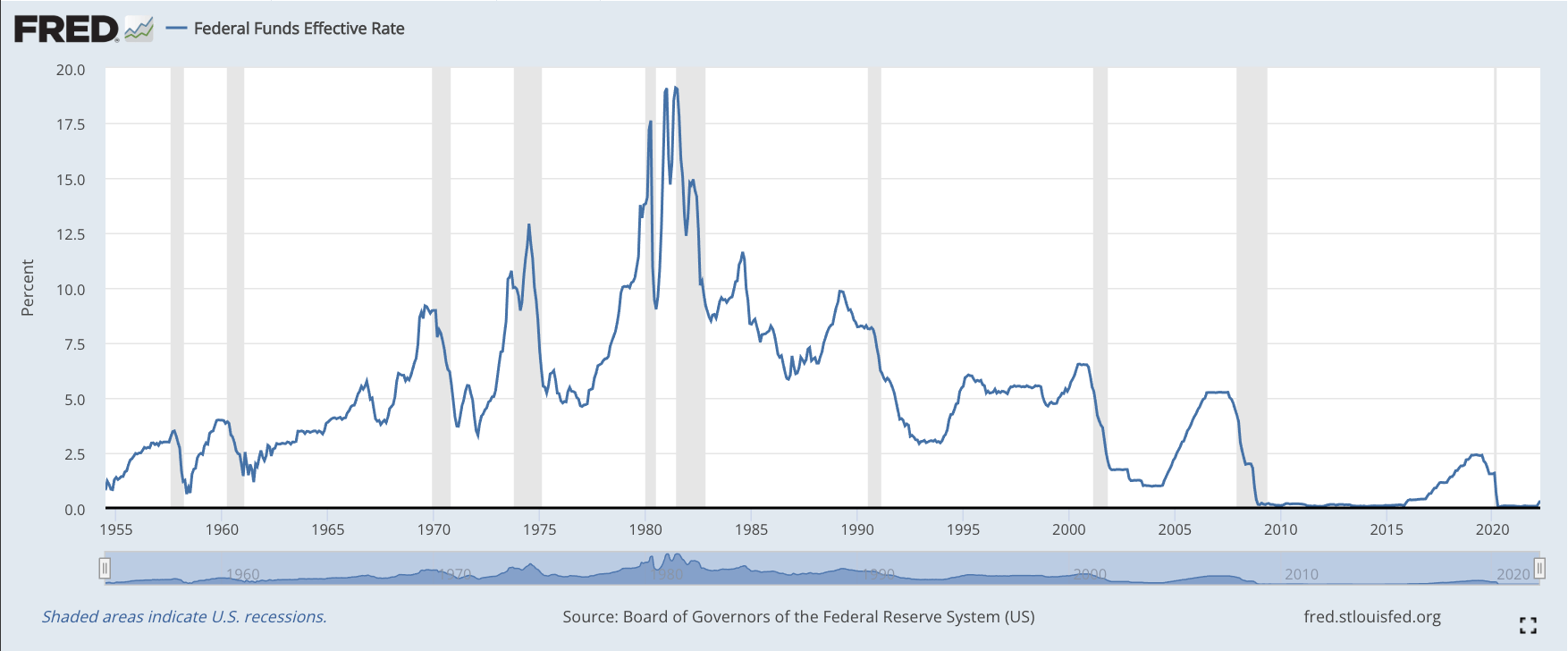

Although the federal funds rates have stayed relatively low over the past decade, the rate was as high as 20% in the early 1980s.3 The Fed dropped rates to zero in March 2020, as the COVID-19 pandemic brought the U.S. economy to a halt. Rates hovered near zero for the better part of two years until the Fed increased them at its March 2022 meeting.

Snapshot of Federal Funds Rates Through the Decades

Source: Macrotrends. “Federal Funds Rate – 62 Year Historical Chart.” https://www.macrotrends.net/2015/fed-funds-rate-historical-chart. Accessed May 11, 2022.

For some economists, the Fed waited too long to raise rates. The Consumer Price Index (CPI), a primary market for inflation, had risen to 7.9% by February 2022 and was still climbing.4 The April CPI reading came in at 8.3%, immediately on the heels of the Fed’s second rate increase.5

What does the federal funds rate have to do with inflation? Remember that low rates spur the economy — and higher rates slow it down. If the Fed raises rates, it will discourage more borrowing and consumers and companies will buy less, resulting in less liquidity and (hopefully) decreasing inflation.

The big question for the Fed now is whether or not to get more aggressive with its rate increases in an attempt to bring down inflation. Although Chairman Powell said the committee is not considering a 75-basis-points hike in June or July, it’s not entirely off the table. In an interview following the Fed’s May meeting, Cleveland Fed President Loretta Mester said, “We don’t rule out 75(%) forever. When we get to that point in the second half of the year, if we don’t have inflation moving down, we may have to speed it up.”6

Federal Funds Effective Rate Since 1955

Source: FRED. “Federal Funds Effective Rate.” https://fred.stlouisfed.org/series/FEDFUNDS. Accessed May 11, 2022.

The Impact of Rising Rates

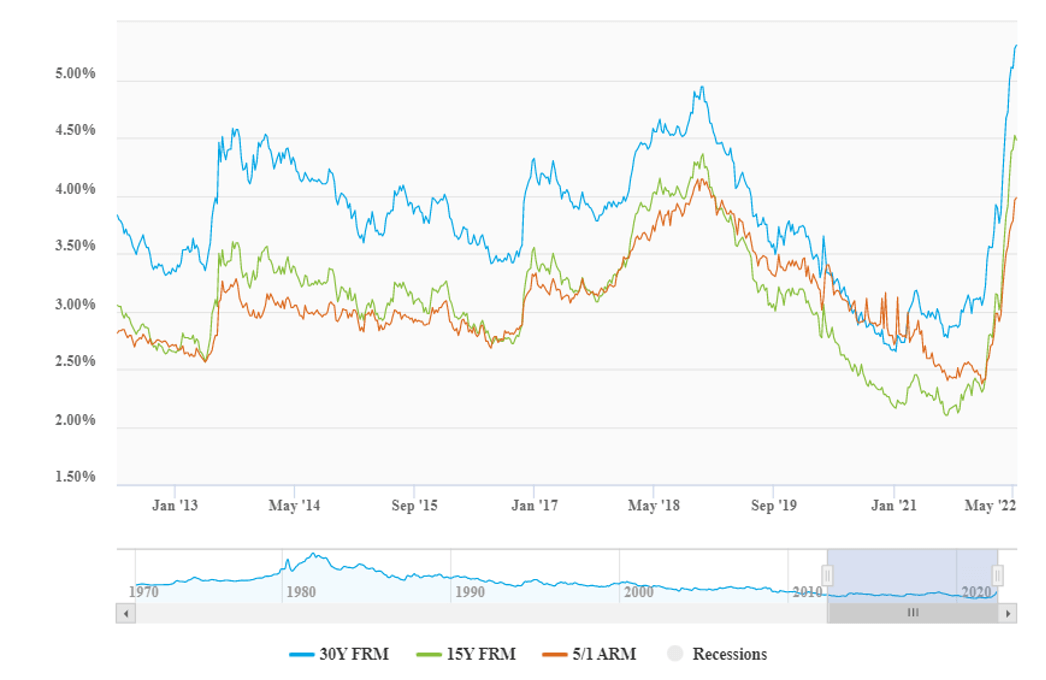

As the federal funds rate rises, banks also will increase interest rates for personal and commercial loans. The U.S. is already seeing this reflected in mortgage rates; the average interest rate on a 30-year fixed mortgage was 2.68% in December 2020 and hit 4.98% in April 2022.7

Mortgage rates over the past decade

Source: Freddie Mac. May 12, 2022. “Mortgage Rates Continue to Increase.” https://www.freddiemac.com/pmms. Accessed May 12, 2022.

Consumers also pay more for credit card purchases, car loans and other personal loans they may take out, such as a home equity loan or line of credit. For investors, rising rates can take a chunk out of company earnings, resulting in potentially lower returns. Bond prices — which move inversely with interest rates — can also be negatively impacted, particularly bonds with longer maturities.

Final Thoughts

So what strategies can consumers take to help protect their savings and maintain their lifestyle in a rising-interest-rate environment? Here are a few tips:

- Evaluate big purchases. If you’ve been thinking about a big purchase — such as a car or home — you may want to lock in your rate before they go higher. Otherwise, you may end up paying more for the same item.

- Invest wisely. Look for assets that have historically performed well when interest rates rise. For example, commodities tend to outperform in periods of rising interest rates, as the price of raw materials often drops when rates increase.8

- Consider shorter bonds. If you’re looking for ways to generate income, short- and medium-term bonds are less sensitive to rate increases. The downside? You give up higher income-earning potential than what’s available in longer-term bonds.

Rising interest rates can impact your financial plan due to decreased income through investment earnings and increased spending. If you’re concerned about rising rates and their potential impact on your retirement, reach out to your financial professional. He or she can help you find opportunities to not just survive but potentially thrive when rates rise.

1 James Chen. Investopedia. May 6, 2022. “Federal Funds Rate.” https://www.investopedia.com/terms/f/federalfundsrate.asp#:~:text=The%20term%20federal%20funds%20rate,reserves%20to%20each%20other%20overnight. Accessed May 11, 2022.

2 Gertrude Chavez-dreyfuss. Reuters. May 5, 2022. “U.S. rate futures price in 75% chance of 75 bps Fed hike in June.” https://www.reuters.com/business/finance/us-rate-futures-price-75-chance-75-bps-fed-hike-june-2022-05-05/#:~:text=Finance-,U.S.%20rate%20futures%20price%20in%2075%25%20chance%20of,bps%20Fed%20hike%20in%20June. Accessed May 11, 2022.

3 Macrotrends. “Federal Funds Rate – 62 Year Historical Chart.” https://www.macrotrends.net/2015/fed-funds-rate-historical-chart. Accessed May 11, 2022.

4 U.S. Bureau of Labor Statistics. March 15, 2022. “Consumer prices for food up 7.5 percent for year ended February 2022.” https://www.bls.gov/opub/ted/2022/consumer-prices-for-food-up-7-9-percent-for-year-ended-february-2022.htm#:~:text=The%20Consumer%20Price%20Index%20rose,month%20advance%20since%20July%201981. Accessed May 11, 2022.

5 U.S. Bureau of Labor Statistics. May 11, 2022. “Consumer Price Index Summary.” https://www.bls.gov/news.release/cpi.nr0.htm. Accessed May 11, 2022.

6 Trading Economics. “United States Fed Funds Rate.” https://tradingeconomics.com/united-states/interest-rate. Accessed May 11, 2022.

7 Freddie Mac. “30-Year Fixed-Rate Mortgages Since 1971.” https://www.freddiemac.com/pmms/pmms30. Accessed May 11, 2022.

8 Mark P. Cussen. Investopedia. March 15, 2022. “How to Prepare for Rising Interest Rates.” https://www.investopedia.com/articles/basics/10/protect-portfolio-from-interest-rates.asp. Accessed May 11, 2022.

This content is provided for informational purposes. It is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security. Individuals are encouraged to consult with a qualified professional before making any decisions about their personal situation. The information and opinions contained herein provided by third parties have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management. Neither AEWM nor the firm providing you with this report are affiliated with or endorsed by the U.S. government or any governmental agency. Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IARs) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM. Information regarding the RIA offering the investment advisory services can be found at http://brokercheck.finra.org.

5/22-2200106