Overview

Tax-minimizing strategies are available to everyone, not just billionaires. There are many ways to help reduce your tax bill on investment gains and income — all perfectly legal. It’s a matter of investing in specific types of holdings in specific types of accounts for specific types of goals.

With that said, it’s important to remember that taxes are but one factor you should consider when building an investment portfolio. However, if one of your goals is to minimize taxes — particularly to accumulate wealth over a long time frame — this may be the primer for you.

“The importance of taxes in your investment strategy will depend on your situation, including your tax rate. The higher your marginal tax rate, the more value there is in pursuing an investment strategy that factors taxes into your decision-making process.”1

Contribute to Tax-Advantaged Accounts

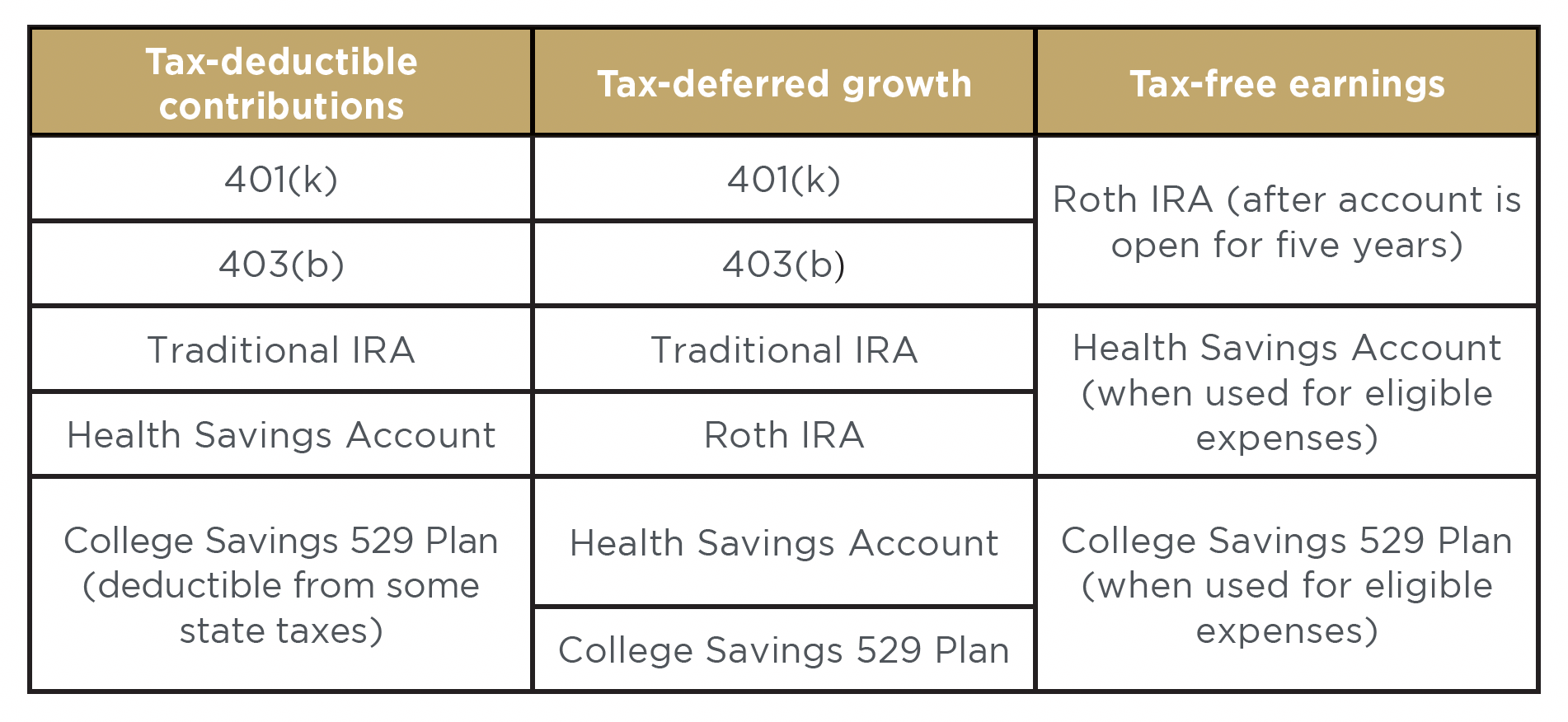

There are several types of tax advantages for investors:

• Tax-deductible contributions — subtracted from current income before taxes are taken out

• Tax-deferred growth — your investment grows tax-free until you take distributions in retirement, when investors are typically in a lower tax bracket

• Tax-free earnings — you never have to pay taxes on gains as long as you follow specific guidelines

This table offers examples of investment accounts that enjoy these tax advantages:

Account-Specific Asset Allocation

The type of account you invest in isn’t just important for tax advantages; it should also be appropriate for the specific financial goal. For example, a young adult saving for a down payment on a house may not want to use a tax-deferred growth account because she’ll likely want that money before retirement age. If she makes an early withdrawal, she’ll trigger significant tax penalties.

By dividing assets among different types of accounts, investors have the flexibility to tap gains for short-term goals while being more tax-efficient for longer-term goals. Since retirement is often several decades away, investing money with tax-deductible contributions in a tax-deferred growth account enables money to compound unencumbered by taxes over a long term.

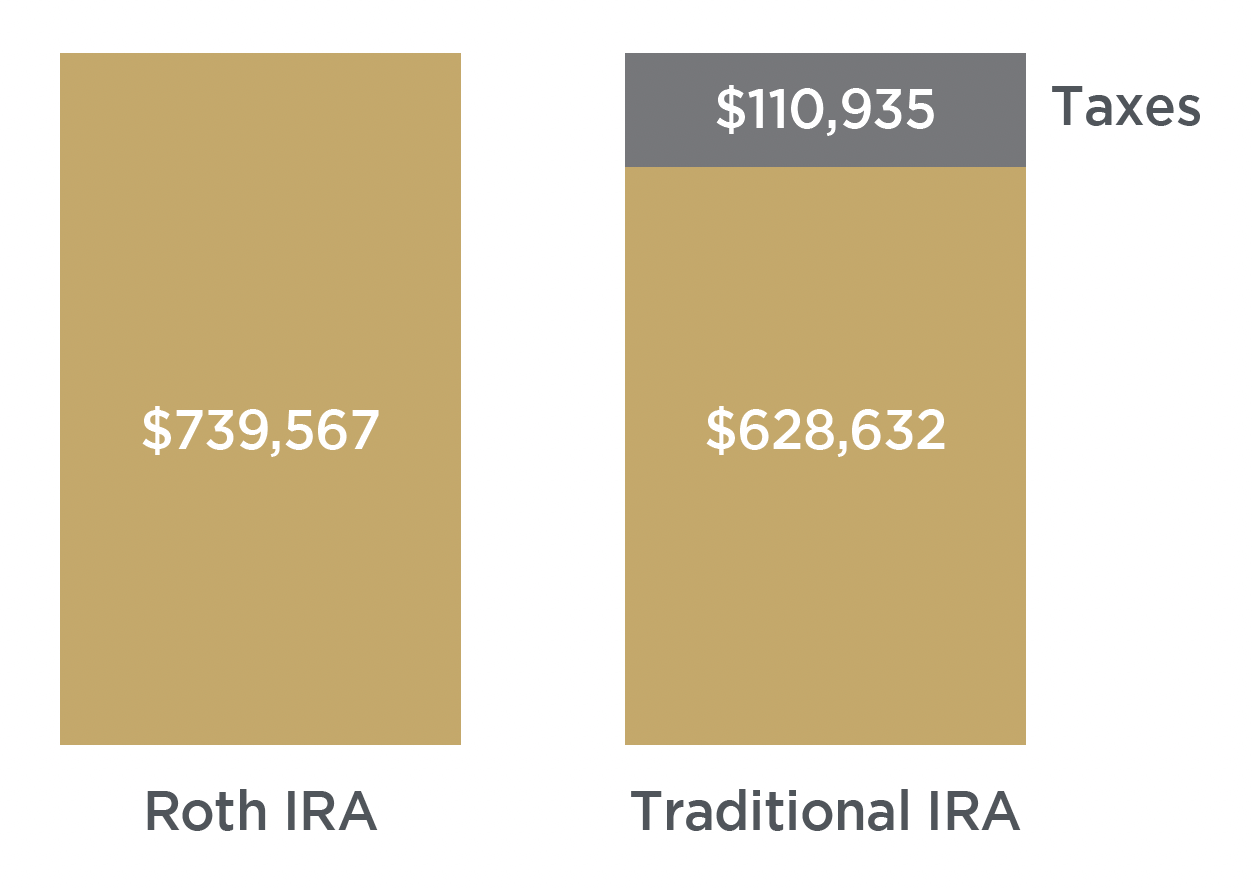

A Tale of Two IRAs

This illustration assumes a $5,000 investment each year for 35 years, with a 7% average annual return. With the Roth IRA, the investor gets to keep the total return. The traditional IRA, on the other hand, requires that the investor pay a total of more than $110,000 in taxes when the money is withdrawn, which substantially reduces his total return.2

A Roth account is generally preferable to a taxable account due to its qualified tax-free withdrawals. It also may be preferable to a tax-deferred account if the investor’s income tax bracket is expected to be higher once she’s in retirement. However, when an investor’s tax rate is likely to be lower or remain the same in retirement, a tax-deferred account will often come out ahead.

Be aware, though, that even with a long-term goal like retirement, it’s important to manage your tax liability. One way to do this is to diversify retirement funds across both tax-deferred and tax-free accounts, such as a 401(k) plan and a Roth IRA.

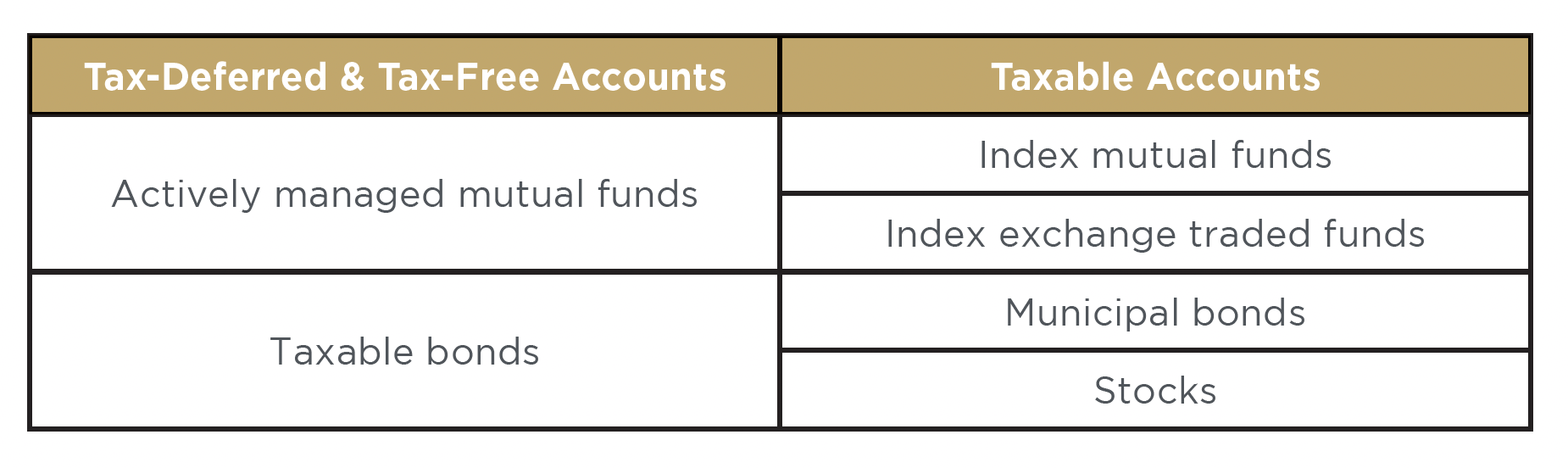

Asset Location

In addition to pairing accounts with goals, consider which types of investments are best suited for different accounts. Investments that are not inherently tax efficient may be more appropriate in a tax-deferred account, while those that are tax efficient may be more useful in taxable accounts. This table provides examples of assets best suited for different accounts:3

For example, a Roth IRA is a good vehicle for investing in high-growth-potential securities because you can hold on to them for a long time to maximize performance — but all of the gains may be distributed tax free. By the same token, a Roth is also appropriate for high-turnover growth strategies so you don’t trigger short-term capital gains as you would in a taxable account.

A taxable account is a good vehicle for investments with inherent tax benefits, such as municipal bonds that are exempt from federal and state income taxes. Otherwise, their tax benefit would be wasted in a tax-advantaged account.4

Tax-Efficient Funds

When seeking to optimize after-tax returns, it’s important to consider each investment option for its inherent tax efficiency. For example, mutual funds are a convenient investment option because you can diversify money across a number of different holdings. However, actively managed mutual funds tend to trade assets more often in an effort to maximize return potential and meet the fund’s objectives. This, in turn, can trigger taxes on an ongoing basis. According to Morningstar, the annual after-tax return for the average mutual fund tends to be about 2% less that than its pretax return.5

If reducing taxes is your focus, it may be more prudent to invest in index mutual funds and index exchange traded funds. Because they are not actively managed but rather designed to track a certain index, they feature less turnover and, therefore, lower taxes.

There are also tax-managed stock funds that are actively managed to reduce taxes compared to other stock funds. However, the extra element of tax management typically means they charge a higher fee, so consider whether the higher expense is worth the lower tax bill.

Tax-exempt bond funds maximize after-tax returns, but they pay lower interest rates, so it may be worth considering whether the lower yield is preferable to a taxable bond.6 Also note that while certain municipal bonds pay out interest income that is tax-free at the federal level, they may be subject to taxes at the state and local level, as well as the federal alternative minimum tax. Moreover, investors could owe taxes on capital gains due to fund trades or through their own share redemptions.

Offset Gains

Often, the best time to assess your investment tax strategy is year-end. If you’ve sold holdings for substantial gains that will trigger capital gains taxes, one way to help offset those taxes is to sell securities that have lost value — a strategy known as tax-loss harvesting. When capital losses total more than your capital gains for the year, you may claim up to $3,000 in deductions in order to reduce your taxable income. If your losses are greater than the deduction limit, you can even carry over the remainder losses to the next year’s tax return.7

If you are interested in selling winners and losers to mitigate your calendar year tax liability, these transactions must be fully completed by Dec. 31. Also note that if you sell shares for a loss and then buy back into that position within 30 days, you’ll run afoul of the “wash-sale rule.” This is when an investor purchases a “substantially identical” security within 30 days of a loss sale, which negates the losses you can claim on your tax return.8 It’s usually a good idea to consult with an experienced investment or tax advisor before deploying this strategy.

Mindful Withdrawal Strategies

As you near retirement, consider whether your income tax rate will increase or decrease when developing a long-term distribution strategy. For example, if you expect your tax rate to be lower, the general recommendation is to withdraw from tax-free accounts first, such as a Roth IRA, then tap tax-deferred accounts such as a 401(k) and traditional IRA.

If you expect your tax rate to be higher once you retire, the more tax-efficient route may be the opposite: Draw down from tax-deferred accounts first and then tap tax-free accounts.9

Philanthropic Strategies

And finally, the IRS offers certain tax advantages to the philanthropic-minded in order to encourage and reward charitable giving. For example:10

• You may claim cash donations (up to certain limits) as a deduction when you itemize your tax return.

• Consider donating highly appreciated securities, such as individual stocks, mutual funds or ETFs to organizations that accept investment gifts. This way, you can make a contribution without having to cash in an investment and pay capital gains on the earnings — and neither does the charity.

• Investors who are at least age 70 ½ may instruct their IRA administrator to make direct payouts to qualified charities totaling up to $100,000 a year. This qualified charitable distribution will also count toward any required minimum distributions. As long as the check is paid directly to the qualified charity, the distribution is not reported on the account owner’s taxable income.

Final Thoughts

Let’s face it, the goal of any investment is to earn more money. But the more money investors accumulate, the more Uncle Sam takes his share. However, you can pay taxes upfront (on your income), as you need it, or on the back end (when distributed in retirement). When and how you receive investment earnings will determine how big your tax bill will be.

That’s why it’s important to work with an experienced financial professional and tax advisor to create a customized strategy to maximize your after-tax returns.

1 Roger Young. T. Rowe Price. June 7, 2021. “How to Make the Most of Your Savings Using a Tax-Efficient Approach.” https://www.troweprice.com/personal-investing/resources/insights/how-to-make-most-of-your-savings-using-tax-effficient-approach.html. Accessed Oct. 11, 2021.

2 Bankrate. 2021. “Roth vs. traditional IRA calculator.” https://www.bankrate.com/retirement/calculators/roth-traditional-ira-calculator/. Accessed Oct. 11, 2021.

3 Jessica McBride. Vanguard. Feb. 18, 2021. “6 tax-saving strategies for smart investors.” https://investornews.vanguard/6-tax-saving-strategies-for-smart-investors/. Accessed Oct. 11, 2021.

4 Roger Young. T. Rowe Price. June 7, 2021. “How to Make the Most of Your Savings Using a Tax-Efficient Approach.” https://www.troweprice.com/personal-investing/resources/insights/how-to-make-most-of-your-savings-using-tax-effficient-approach.html. Accessed Oct. 11, 2021.

5 Ibid.

6 Jessica McBride. Vanguard. Feb. 18, 2021. “6 tax-saving strategies for smart investors.” https://investornews.vanguard/6-tax-saving-strategies-for-smart-investors/. Accessed Oct. 11, 2021.

7 Ibid.

8 Jason Fernando. Investopedia. Oct. 4, 2021. “Wash-Sale Rule.” https://www.investopedia.com/terms/w/washsalerule.asp. Accessed Oct. 19, 2021.

9 Jessica McBride. Vanguard. Feb. 18, 2021. “6 tax-saving strategies for smart investors.” https://investornews.vanguard/6-tax-saving-strategies-for-smart-investors/. Accessed Oct. 11, 2021.

10 Ibid.

This content is provided for informational purposes. It is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security. Individuals are encouraged to consult with a qualified professional before making any decisions about their personal situation. The information and opinions contained herein provided by third parties have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management. Neither AEWM nor the firm providing you with this report are affiliated with or endorsed by the U.S. government or any governmental agency. Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM. Information regarding the RIA offering the investment advisory services can be found at https://brokercheck.finra.org/. 10/21 – 1874612