Overview

As U.S. employers desperately seek workers, millions of mothers remain on the sidelines due to health safety concerns, school quarantines and the fact that child care costs more than many of them earn. And while parents pay more than they can afford, child-care workers can’t live on what they’re paid.

A recent survey found that among working mothers driven out of the workforce due to COVID-19, 70% left voluntarily for caregiving reasons and 30% were laid off. Perhaps of greater concern is that 69% of working mothers plan to remain out of the job market to care for their children. According to analysis by McKinsey & Company, women’s employment levels are not expected to rebound to pre-pandemic levels until 2024.1

Vaccines may have offered a path back to normalcy, but many have not taken that path. As long as the coronavirus continues to spread and there is no vaccine protection for young children, a large number of moms will remain out of the workforce. That sets the stage for a potential crisis in household finances, a setback for gender equality gains and a continuous drag on U.S. and global economic growth.

“The pandemic continues to wreak havoc on people’s careers, but no one has been hit harder than working mothers.” 2

Financial Toll for Women

Gender parity was already at stake before the pandemic. Most mothers take time out of the workforce to, at the very least, recover from childbirth, but many take off a year or more to stay home with their children. With this in mind, it is astounding what a difference a year can make. According to data from the Institute for Women’s Policy Research, taking just one year off from the labor force yields an average reduction of 39% in annual earnings over a 15-year period. Two years out of the workforce can yield a loss of a quarter of a million dollars in income over a woman’s lifetime. The majority of lost money doesn’t come from the year or longer that she remains out of work. Rather, it comes from other lost opportunities resulting from that timeout.3

Lifetime earnings are lost for many reasons, including:

• Income lost while not working

• Future income forgone due to lost promotions, training and other job opportunities

• Lost seniority at work

• When women return to the job market from time off to care for children, studies show that employers tend to regard them differently, such as less committed to their jobs

• Flexible work policies — even working from home full or part time can hurt women because they lose out on workplace exposure and relationship-building opportunities

• Lower overall wages translate into lower Social Security benefits

• Less opportunity to save • Reduced retirement benefits

• Fewer assets to take advantage of long-term compounding

Pandemic Toll

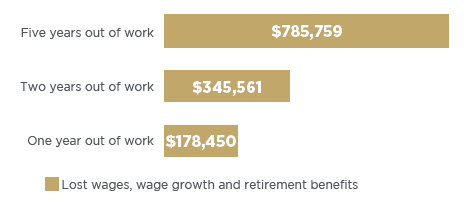

According to analysis by the Center for American Progress, a woman earning the median wage of $47,299 before the pandemic, who returns to full-time work by 2022, could still lose more than $250,000 in income over her lifetime. This assessment is based on lost current earnings (40%), lower future income growth (30%) and reduced retirement benefits (30%). For the average college-educated woman earning the median income of $62,140, the potential losses are even greater, as illustrated in the accompanying chart.4

Long-Term Cost to College-Educated Women:

Median Salary $62,140

Data assumes the worker was 30 years old when she stopped working because of the pandemic; once back at work, made typical contributions to an employer-sponsored retirement savings plan that earned 4% a year after inflation; then left the workforce for good at age 67, spending 20 years in retirement.

Dependent Care and Other Mom-Friendly Benefits

According to Pew Research, 46% of U.S. households are composed of families in which both parents work full time. And yet, only 9% of employers provide or are considering providing child-care subsidies.5

This means the vast majority of American families are on their own when it comes to finding, vetting and paying for child care while parents are at work. Therefore, it’s important for employers to consider more family-friendly benefits that will help women remain in the workforce over the long term.

The following are some of the most popular benefits among workers with children, elderly parents or those who want to start a family:

• Flexible hours and work-from-home options

• Work scheduling: Fixed hours (e.g., hourly workers), compressed workweeks (e.g., work 40 hours in 4 days); staggered or reduced schedules so workers can spend more daytime hours with children

• Job sharing

• More robust paid maternity and paternity benefits

• Tax-advantaged dependent care reimbursement accounts • Extended paid vacation time

• Provide a centralized platform for workers to research and even crowd-source references for caregiving resources

• Referral, navigation or placement resources • Backup care resources • On-site daycare or pop-up, on-site day care for school holidays/teacher workdays

• A care cohort or co-op, in which workers share a caregiver and the cost of the service

• Tutoring or homework help for school-age children

• Homemade dinner order/take-home options

• Errand-running services

• Virtual medicine benefit coverage so workers can consult with a physician without leaving work

• Company discounts for tools and devices to help caregivers manage their responsibilities, such as caregiver robots for basic functions and keeping seniors company; interactive audio devices (e.g., Amazon’s Alexa) to help an elderly parent order common household goods; smartphone apps to help caregiver workers keep track of parental finances and pay bills and set up alarms on their cell phones to remind seniors when to take medications; home video monitoring devices to keep an eye on their charges — both the elderly and latchkey kids — from work

• Fertility benefits, such as in-vitro fertilization, infertility diagnosis and medication, egg freezing, donor eggs or embryos, surrogacy and adoption assistance

Commensurate Pay

The gender gap in pay has always existed, but it was on a path trending higher — until the pandemic hit. In 2019, women earned an average of 83% that of men, although a wider gap existed for Black and Hispanic women. However, the pandemic has likely increased that gender wage gap by five percentage points. According to the National Bureau of Economic Research, women aren’t expected to recover to 2019 levels for another 20 years.6

The Path Forward: Human Infrastructure

The current controversy in Washington comes down to what constitutes “infrastructure.” There is bipartisan agreement that our bridges, roads and transit systems are in drastic need of repair and updating. There’s even some consensus that, moving forward, infrastructure spending also should include broadband access, green technologies and renewable energy.

However, the debate is largely centered on whether paid family/medical leave and subsidized child care should be funded as part of an infrastructure spending package.

The current Family and Medical Leave Act offers job security to eligible employees who take time off (usually unpaid) to care for a newborn or ill family member. However, only about 20% of employees in the private sector enjoy this privilege. President Biden has proposed extending this policy to give all workers up to 12 weeks of paid family and medical leave, which would be paid for by the government, not individual employers. This provision is included in his “Build Back Better” $3.5 trillion “human infrastructure” bill currently being debated in Congress.7

The bill defines human infrastructure as part of the critical infrastructure the country needs to get people back to work. Proponents claim that issues like child care, home care and paid leave are all obstacles that will continue to weigh on Americans — no matter how many bridges or light rail systems we build. Today, child care alone can cost a family up to 20% of their household income.8 And yet, the pay for caregivers is so low that they can’t afford a living wage working that job.

This has been an ongoing problem for households since women joined the workforce in droves. However, our beleaguered child-care system broke down entirely during the pandemic, when closed schools, day care centers and even quarantined grandparents were no longer an option.

Universal Preschool Proposal

In addition, President Biden has proposed longer-term child-care infrastructure via the $1.8 trillion American Families Plan. It includes provisions for universal preschool, an extension of the child-tax credit expansion, and calls for a 7% cap on household income for the family’s share of child-care spending for low- and middle-income families. Today, the U.S. spends less on early childhood education than most other developed countries. For example, subsidized preschool in countries like Sweden and Finland means that parents pay only $30 to $330 a month, based on municipality, household income and family size.

Note that government-subsidized child care is not unprecedented in the U.S. Back during World War II, when it was imperative for women to replace men in the workforce, the government invested $1 billion (adjusted to today’s dollars) for subsidized child care. Households paid between $0.50 and $0.75 per child, per day, for state-sponsored child-care centers.9

Economic Reality

If the U.S. does not deploy government-subsidized solutions that will allow more mothers to enter the workforce, economic growth will likely continue to lose ground. Since the onset of the pandemic, the National Partnership for Women & Families attributes a $97 billion loss in GDP to the decline in women’s labor force participation. In states like Texas, Florida, Nevada and Arizona, prime-age women’s labor force participation rates have dropped below 75%.

If the U.S. regained labor force participation for prime-age women at rates similar to that of women in Canada, Germany and the United Kingdom, we could add up to $650 billion per year to the overall economy.10

“If there’s a retirement crisis for women in 30 years, the pandemic will be where it all got started.” 11

Final Thoughts

With one parent still out of the workforce, many families are struggling to make ends meet. However, the struggle may seem worth it as children and elderly parents get the attention they need and, on the whole, the family continues to survive.

The problem that will eventually emerge is when unemployed women approach retirement. They have long been disadvantaged in this regard, as women generally earn less than men in their lifetimes, have less saved for retirement, receive lower Social Security payouts (i.e., $1,154 vs. $1,466 a month, on average) — and yet they tend to live at least five years longer than men.12 Thus, the poverty women tend to face in retirement will likely be exacerbated in the future by the devastating impact of the pandemic.

Thus, it is important for households to do more than just make ends meet during this trying time. They need to think about the long-term future for both spouses — but perhaps particularly for moms. Those who want to work need to find suitable child-care solutions so that they can contribute to retirement plans, earn higher entitlement benefits and adequately prepare for a retirement that may or may not include their spouse.

This is not just a woman’s problem, it is a family issue, it is a national issue and an economic priority. Consult with an experienced financial professional for help finding ways to maximize income and current savings to ensure long-term financial security.

1 Alyssa Place. Employee Benefit News. June 15, 2021. “Enough is enough: Majority of working moms aren’t planning on returning to work.” https://www.benefitnews.com/news/majority-of-working-moms-wont-return-to-work. Accessed Sept. 28, 2021.

2 Ibid.

3 Emily Peck. Newsweek. May 26, 2021. “Exclusive: Pandemic Could Cost Typical American Woman Nearly $600,000 in Lifetime Income.” https://www.newsweek.com/2021/06/11/exclusive-pandemic-could-cost-typical-american-woman-nearly-600000-lifetime-income-1594655.html. Accessed Sept. 28, 2021.

4 Ibid.

5 Amanda Schiavo. Employee Benefit News. June 15, 2021. “Investing in childcare benefits creates a more equitable workforce.” https://www.benefitnews.com/news/investing-in-child-care-benefits-creates-a-more-equitable-workforce. Accessed Sept. 28, 2021.

6 Emily Peck. Newsweek. May 26, 2021. “Exclusive: Pandemic Could Cost Typical American Woman Nearly $600,000 in Lifetime Income.” https://www.newsweek.com/2021/06/11/exclusive-pandemic-could-cost-typical-american-woman-nearly-600000-lifetime-income-1594655.html. Accessed Sept. 28, 2021.

7 Katie Kindelan. ABC News. Sept. 28, 2021. “Congress close to passing paid family and medical leave: Here’s what it would mean.” https://abc7news.com/congress-close-to-passing-paid-family-and-medical-leave-heres-wha/11057308/. Accessed Sept. 28, 2021.

8 Kerry Kavanaugh. Boston 25News. Sept. 22, 2021. “One-on-one with MA Rep. Katherine Clark on ‘human infrastructure’ and what’s at stake.” https://www.boston25news.com/

news/health/one-on-one-with-ma-rep-katherine-clark-human-infrastructure-whats-stake/MXC5WTD2PVAZJPGBQVMOHJAJYE/. Accessed Sept. 28, 2021.

9 Heather Marcoux. Motherly. Sept. 13, 2019. “Would it ever be possible to have universal childcare in the United States?” https://www.mother.ly/life/news/news-trending/can-the-united-states-have-universal-childcare. Accessed Sept. 28, 2021.

10 Amanda Novello. National Partnership for Women & Families. July 2021. “The Cost of Inaction: How a Lack of Family Care Policies Burdens the U.S. Economy and Families.” https://www. nationalpartnership.org/our-work/resources/economic-justice/other/cost-of-inaction-lack-of-family-care-burdens-families.pdf. Accessed Sept. 28, 2021.

11 Emily Peck. Newsweek. May 26, 2021. “Exclusive: Pandemic Could Cost Typical American Woman Nearly $600,000 in Lifetime Income.” https://www.newsweek.com/2021/06/11/exclusive-pandemic-could-cost-typical-american-woman-nearly-600000-lifetime-income-1594655.html. Accessed Sept. 28, 2021.

12 Ibid.

This content is provided for informational purposes. It is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security. Individuals are encouraged to consult with a qualified professional before making any decisions about their personal situation. The information and opinions contained herein provided by third parties have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management. Neither AEWM nor the firm providing you with this report are affiliated with or endorsed by the U.S. government or any governmental agency. Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of

the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM. Information regarding the RIA offering the investment advisory services can be found at https://brokercheck.finra.org/. 10/21 – 1855276 For financial professional use only.